"Prepare for the Union Budget 2026 special trading session. Comprehensive Nifty 50 analysis: Support at 25,230, resistance at 25,460, and highest probability outlook."

The scheduling of the Union Budget on February 1, 2026, coinciding with a Sunday, introduces a rare structural anomaly into the Indian capital markets. For the first time since 2017, the Ministry of Finance has chosen a weekend to present its annual financial statement, compelling the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE) to conduct a special live trading session. Heading into this session, the market is navigating a complex interplay of persistent foreign fund outflows, record-high domestic currency weakness, and a global geopolitical landscape characterized by shifting interest rate regimes.

Final Technical Synthesis: Nifty 50 and India VIX

NIFTY50 30/01/2026

Join Telegram

The latest technical charts indicate that the Nifty 50 is entering the Budget session at a critical "make-or-break" juncture. The index has shown a marginal decline of -9.75 points (-0.04%) to close at 25,315.80, sitting right at the bottom of its Central Pivot Range (CPR).

Nifty 50 Price Action and CPR

The Nifty 50 Index is currently pinned within a tight consolidation zone. The Central Pivot Range (CPR) for the session is positioned between 25,309 and 25,38. A close below 25,309 on Sunday would signal a bearish breakdown, whereas a move above 25,382 is required to reclaim bullish momentum.

- Immediate Support: S1 is marked at 25,231.65. A breach of this level will likely lead the index to test the 200-day DEMA zone at S2 (25,161.25)

- Overhead Resistance: R1 is at 25,459.6. Massive selling pressure is expected at R2 (25,530) and the 100-day DMA hurdle at 25,600.

- Volume Analysis: The volume bars at the close of January 30 show a sharp spike to 11.51M, indicating heavy institutional positioning and "position squaring" before the high-event risk.

Derivative Positioning: OI and Change in OI

The Options Chain data reveals a market that is heavily capped on the upside but seeking a firm floor.

- Resistance (Call Side): There has been aggressive Call writing (Red Bars) at the 25,400, 25,500, and 25,600 strike. The 25,400 strike has the highest Open Interest, acting as a "ceiling" for any budget-day rally.

- Support (Put Side): Put writing (Green Bars) is concentrated at 25,300, 25,200, and 25,000. The 25,300 strike is the primary battleground, where significant Put OI addition suggests traders are betting on this level to hold.

- Max Pain: The current "Max Pain" strike for the Nifty 50 is calculated at 25,418.9 . This suggests that option sellers are incentivized to keep the index near 25,400 to minimize payout.

Join Telegram

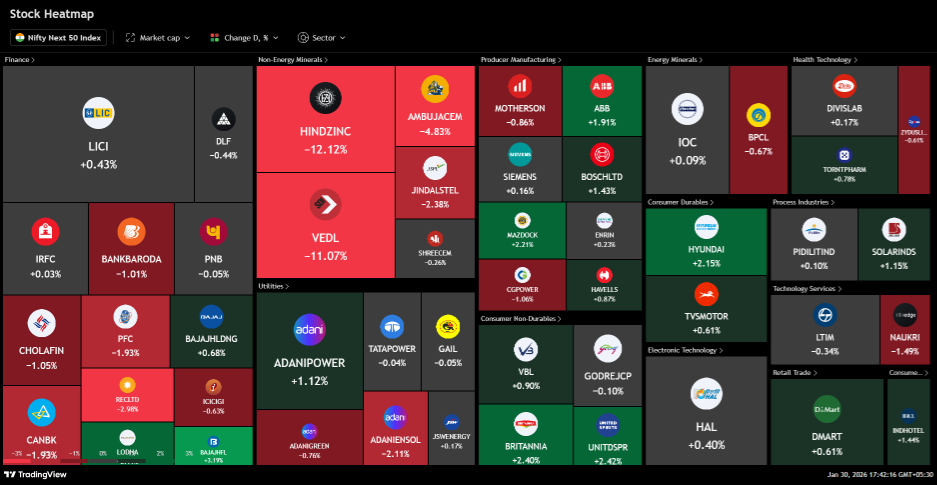

Granular Sectoral Analysis and Heatmap Deep-Dive

The heatmaps across the Nifty 50, Next 50, and Next 500 showcase a stark divergence between globally exposed sectors and domestic structural plays.

Nifty 50: Metal and Finance Under Pressure

The Nifty 50 heatmap shows deep red across the Metals and Banking sectors.

- Metals: This remains the weakest pocket, with Hindalco (-6.00%) and Tata Steel (-4.54%) facing extreme selling. This is likely due to "Trump Tariff" threats and a global slowdown in base metal prices.

- Finance: Private banking heavyweights like ICICI Bank (-2.07%) and HDFC Bank (-0.67%) are dragging the index.

- Safe Havens: Consumer Non-Durables are providing a cushion, with Nestle (+3.46%), Tata Consumer (+2.41%), and ITC (+1.11%) showing strength.

Nifty Next 50 and Next 500 Trends

The broader market is witnessing a "liquidity flush" in specific stocks.

- Next 50 Weakness: Extreme volatility is visible in HindZinc (-12.12%) and VEDL (-11.07%).

- Next 50 Strength: Consumer discretionary and liquor stocks like Britannia (+2.40%) and United Spirits (+2.42%) are attracting defensive flows.

- Next 500 Overview: The Nifty 500 heatmap confirms that while the headline index is flat, the underlying market breadth remains weak, with 2,533 declining shares against 1,706 advancing on the BSE.

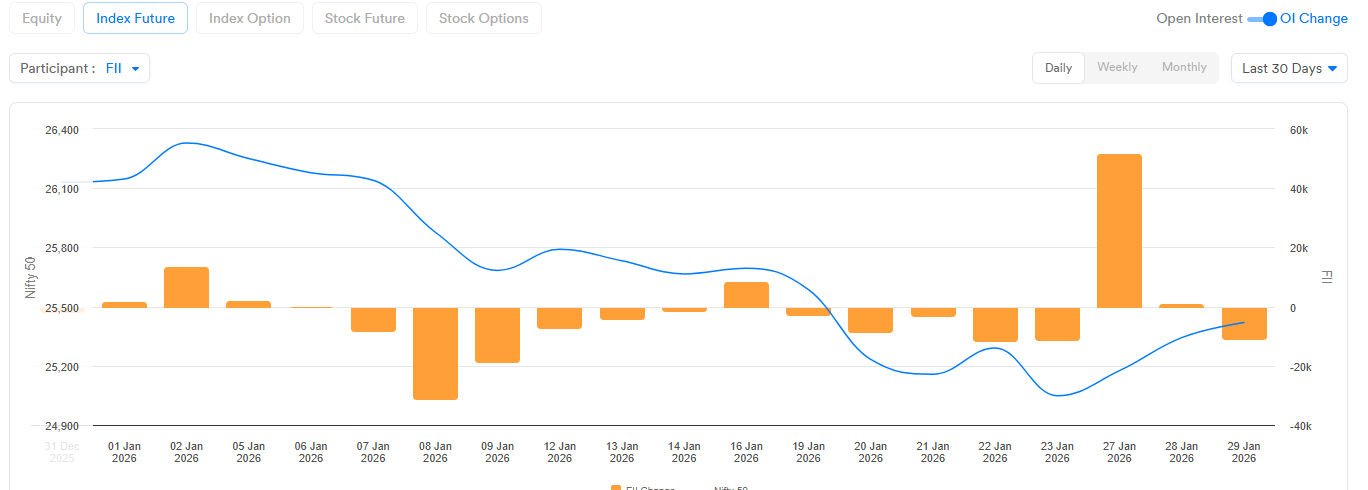

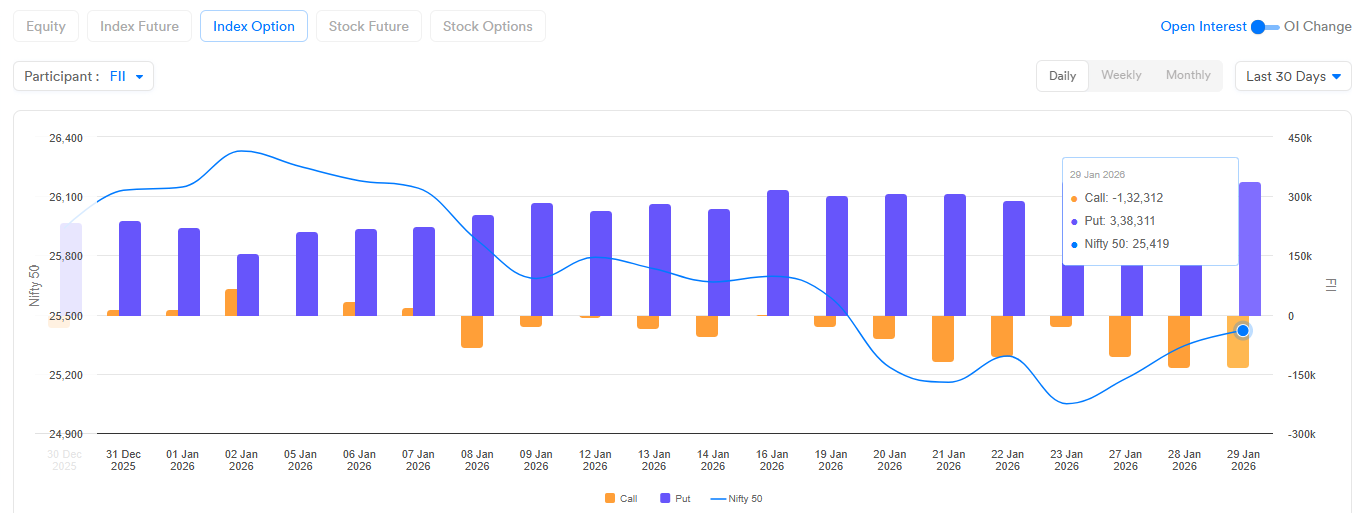

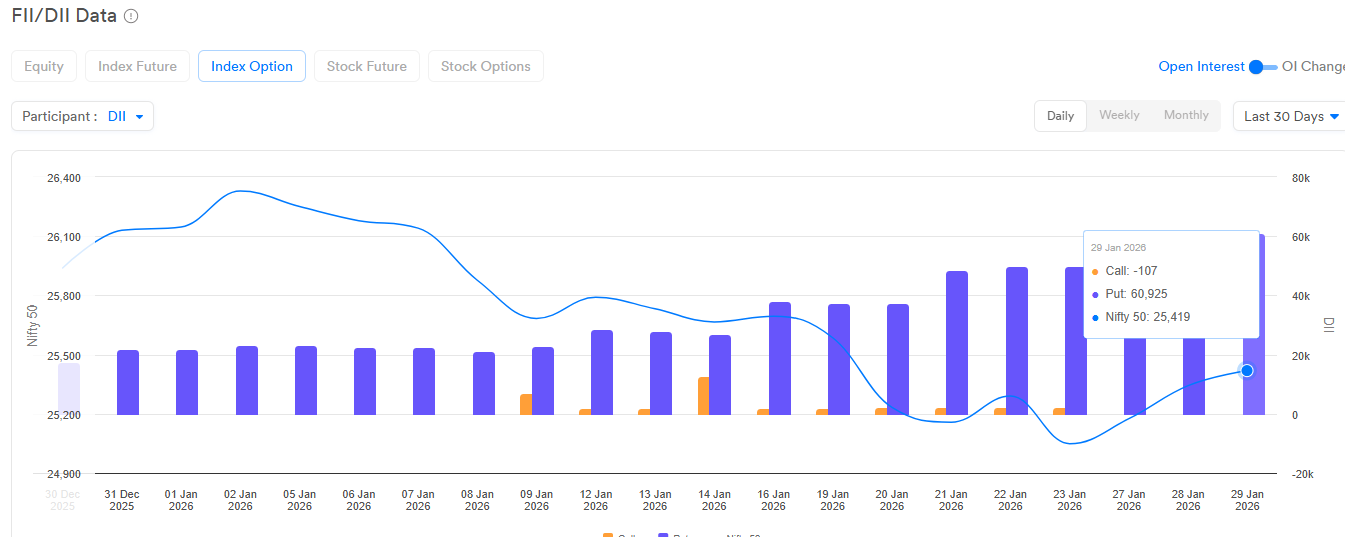

FII and DII Activity Analysis

Index Future

Index options FII

Index options DII

The "tug-of-war" between foreign and domestic institutions has reached its peak.

- FII Selling: Foreign Institutional Investors continued their selling streak in the cash segment, offloading shares worth ₹393.97 crore on January 29. For the month of January, FII outflows have exceeded ₹43,000 crore. FIIs are currently net short in index futures, indicating a defensive posture.

- DII Support: Domestic Institutional Investors have been the sole market stabilizer, buying equities worth ₹2,638.76 crore on January 29 . DIIs are currently in "absorption mode," picking up high-quality large caps that FIIs are exiting.

| Institution | Net Activity (Jan 29, 2026) | Trend | Bias |

| FII (Cash) | -₹393.97 Cr | Selling | Bearish |

| DII (Cash) | +₹2,638.76 Cr | Buying | Bullish |

| FII (Futures) | Net Short | Cautious | Bearish |

High-Conviction Sectors and Stocks to Watch

Based on current sectoral strength and budget expectations, investors should pivot toward "Build India" and "Dividend Play" themes.

1. Public Sector Enterprises (PSE) & Infrastructure

The PSE space is emerging as the most promising theme, with the Nifty PSE Index showing a structural "Cup and Handle" breakout.

- Focus Stock 1: State Bank of India (SBIN). A primary candidate for a massive dividend hike following the RBI's draft proposal to raise the payout cap to 75%. Target: ₹1,150.

- Focus Stock 2: Bharat Electronics (BEL). A "Make in India" champion with a ₹50,000 crore order pipeline, set to benefit from the expected push in "Drone Shakti" and indigenous defence systems.

2. Capital Expenditure & Power

With a CapEx target expected to exceed ₹12 trillion, infrastructure proxies remain high-priority.

- Focus Stock 1: Larsen & Toubro (L&T). The ultimate proxy for India's capex cycle, showing technical strength with a +3.66% gain.

- Focus Stock 2: Tata Power. Positioned as a green energy powerhouse, perfectly aligned with expected VGF and Renewable Energy (RE) incentives in the budget.

Directional Bias and Final Forecast for February 1

Based on the synthesis of the new technical charts, the battle at the 25,300 Put strike, and persistent FII selling, the highest probability for the Nifty 50 on February 1 is a "Whipsaw" session that ultimately fails to sustain a breakout, likely closing flat to marginally negative.

Directional Reasoning:

- Sell-on-Rise Bias: The massive Call writing at 25,400 and 25,500 acts as a formidable barrier. Unless the Finance Minister announces a "Big Bang" reform (e.g., major capital gains tax cuts), institutional desks will likely use any 100-150 point rally as an opportunity to unload positions.

- The "Gamma Trap": The Nifty is currently trapped between 25,230 (S1) and 25,460 (R1). The index will likely swing violently within this 230-point range during the speech but gravitate back toward the Max Pain level of 25,418 by the close.

- Sunday Session Anomaly: Thinner liquidity and the absence of T+0 settlement mean that price swings could be exaggerated. Investors should avoid chasing the market in the first hour and wait for the "volatility crush" post-speech.

Highest Probability Range: 25,150 – 25,550.

Final Direction: Range-bound with a bearish tilt on recoveries.

Strategic Recommendations:

- For Intraday Traders: Avoid long positions if the index fails to cross and sustain above 25,450. Look for "Short Build-up" opportunities if the 25,300 Put support shows signs of unwinding.

- For Positional Investors: Use budget-day volatility to accumulate structural winners like SBIN and BEL, as the post-budget week historically delivers returns seven times larger than the day itself.

Join Telegram

Launch your Graphy

Launch your Graphy